The Second Crash: Tips for Negotiating Medical Bills After a Car Accident

A car accident is traumatic enough. Then the bills arrive. Here’s how to navigate the confusing, often overwhelming, world of medical billing and negotiate for a fair outcome.

There’s a unique kind of quiet that follows the screeching tires and shattering glass of a car accident. It’s a moment suspended in time, filled with adrenaline and disbelief. But after the initial shock wears off and you begin the slow, arduous process of healing, a different kind of chaos begins. It arrives in your mailbox, a steady stream of envelopes that feel heavier than they should. This is the second crash: the overwhelming, often confusing, and astronomically expensive wave of medical bills.

Honestly, it’s a part of the experience that no one really prepares you for. You’re dealing with physical pain, emotional trauma, and the disruption of your daily life, and on top of it all, you’re expected to become a financial detective. I’ve talked to friends who felt like they were drowning in paperwork, with bills from the emergency room, the radiologist, the surgeon, and the physical therapist all arriving at different times with different formats and different due dates. It’s a system that feels designed to be confusing, but I’m here to tell you that you don’t have to just accept it.

It’s a little-known fact that medical bills are often negotiable. You have the right to question charges, to ask for discounts, and to ensure you’re not paying for mistakes. It takes a bit of courage and a lot of organization, but taking control of the financial aspect of your recovery is a crucial step in truly moving forward. Let’s walk through how you can approach this daunting task, not as a victim, but as an advocate for your own well-being.

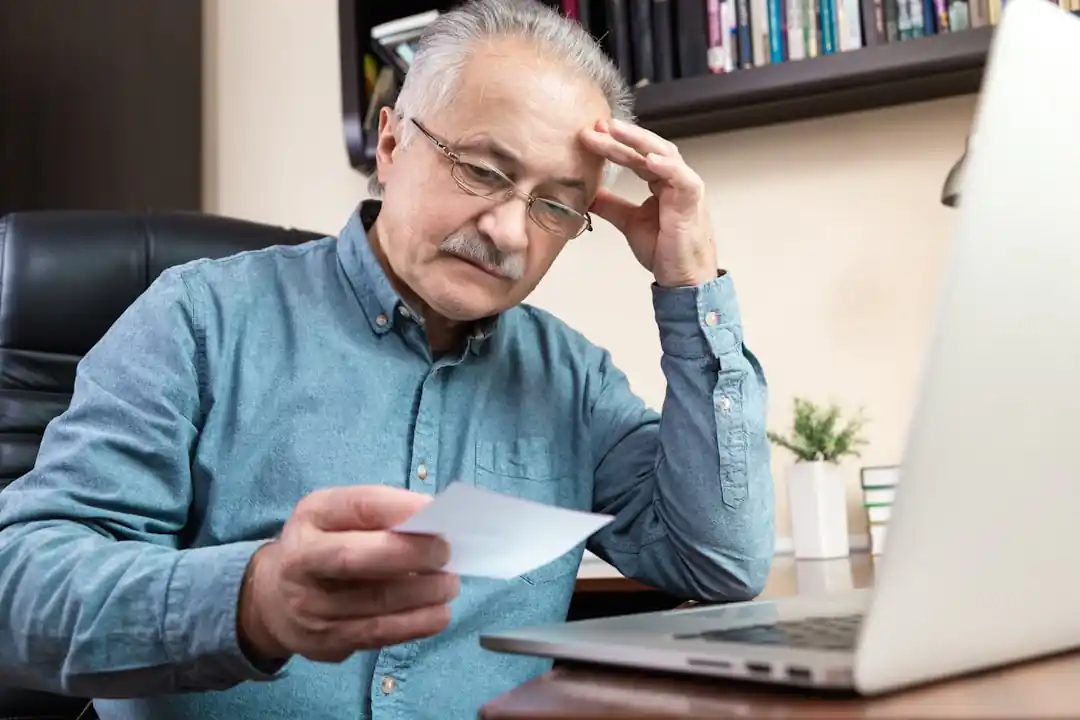

First Step: Become a Master Organizer

Before you can even think about negotiating, you need to know exactly what you’re dealing with. This is where you channel your inner librarian and create a comprehensive file of every single piece of paper related to your accident. This isn’t just about being neat; it’s about building a case. Every document is a piece of evidence that supports your story and your financial situation.

Start a physical binder or a dedicated folder on your computer. In it, you’ll keep copies of the police report, your insurance information, and any correspondence with insurance adjusters. Most importantly, you’ll collect every single medical bill and document. This includes the initial emergency room invoice, bills from individual doctors who may have treated you, pharmacy receipts, and statements from physical therapy or chiropractic sessions. Don’t throw anything away.

For every bill you receive, ask for an itemized statement. This is a critical step. The summary bill you first get often just shows a total, but the itemized version lists every single charge, from a single aspirin to the use of the operating room. This is where you’ll spot errors, and trust me, they are more common than you think. As you gather these documents, create a log. Note the provider, the date of service, the amount billed, what your insurance has paid (if anything), and the outstanding balance. This will give you a clear, at-a-glance overview of your financial exposure.

The Detective Work: Scrutinizing Your Bills for Errors

Now that you have your itemized bills, it’s time to put on your detective hat. You’re looking for mistakes, and there are a few usual suspects that appear time and time again. One of the most common is duplicate billing, where you’re charged twice for the same service. This can happen easily in the chaos of a hospital setting. Compare the dates and service codes carefully. If you see two identical charges, flag it immediately.

Another common error is “upcoding.” This is when a provider bills for a more expensive service than the one you actually received. For example, a simple consultation might be coded as a complex one. While it can be hard for a layperson to spot, if a charge seems wildly out of proportion for the service you remember, it’s worth questioning. Also, look for charges for services you never received. Were you billed for a test that was cancelled? Or for a medication you were never given? It happens.

Finally, check for unbundling. This is when services that should be billed as a single package are broken down into individual charges, which often inflates the total cost. Think of it like being charged separately for the burger, the bun, the lettuce, and the tomato instead of just buying a hamburger. If you see a long list of small charges for a single procedure, it might be a case of unbundling. Don’t be intimidated by the medical jargon. If something looks wrong, it probably is.

The Art of the Ask: How to Negotiate

Once you’ve identified potential errors and have a clear understanding of your bills, it’s time to start negotiating. Your first call should be to the provider’s billing department. Be polite, but firm. Explain that you were in a car accident and are trying to manage the costs. Start by pointing out any clear errors you found. Often, they will correct these without much fuss.

If there are no obvious errors, your next step is to ask for a discount. You’d be surprised how often this works. Many providers are willing to reduce the bill, especially if you offer to pay a lump sum in cash. They would rather get a smaller amount now than have to chase the full amount through collections for months or years. You can ask for the “in-network” or “insured” rate if you’re uninsured. This is the discounted rate they’ve already negotiated with insurance companies, and it’s often significantly lower than the “sticker price” they bill to individuals.

If you have a high-deductible health plan, or if your insurance has denied a claim, you have a strong case for negotiation. Explain your financial situation. You don’t need to share your entire life story, but being honest about your hardship can make a difference. Ask if they have a financial assistance or charity care program. Many non-profit hospitals are required to offer this. The key is to be persistent and to not take no for an answer on your first try.

Knowing When to Call in the Professionals

There’s no shame in admitting when you’re in over your head. If the bills are astronomical, the billing department is uncooperative, or the legal situation with your accident is complex, it might be time to call for backup. A personal injury attorney can be an invaluable asset in these situations. They are experienced in negotiating with both medical providers and insurance companies.

An attorney can often negotiate a much larger reduction than you could on your own. They understand the legal nuances and can use the leverage of a potential lawsuit to get providers to lower their bills. They can also manage the entire process, taking the stress and paperwork off your plate so you can focus on your recovery. Most personal injury lawyers work on a contingency fee basis, meaning they only get paid if you get a settlement or win your case.

The aftermath of a car accident is a marathon, not a sprint. It’s a journey of physical healing, emotional recovery, and, unfortunately, financial navigation. But you don’t have to be a passive passenger on this ride. By being organized, diligent, and assertive, you can take control of your medical bills and ensure that the second crash doesn’t do more damage than the first. You’ve been through enough. You deserve to heal without the crushing weight of unfair medical debt.

You might also like

Your Unshakeable Foundation: Understanding the Most Important Legal Rights for US Citizens

Ever wonder what truly protects you as a American citizen? Let's dive into the fundamental legal rights that form the bedrock of our society, making sure you know your power.

The Ultimate 10-Day Morocco Itinerary: A Journey for the Senses

From the bustling souks of Marrakech to the silent majesty of the Sahara Desert, this 10-day travel guide to Morocco is your ticket to an unforgettable adventure.

From Toy Box to Treasure Chest: A Beginner's Guide to Investing in LEGO Sets

Ever wonder if that childhood hobby could be a serious side hustle? Let's dive into the surprisingly lucrative world of LEGO investing.

A Local's Guide to Navigating the Twin Cities by Public Transit

Ditching the car doesn't mean you're stuck. Here’s a friendly guide to mastering the Minneapolis-St. Paul public transportation system like a pro.

What Are Merchant Services and Why Does My Business Absolutely Need Them?

Diving deep into the world of payment processing. It’s not just about swiping cards; it’s about unlocking your small business's true potential.