Finally Take Control: How to Create a Budget That Actually Works

Feeling like your money has a mind of its own? Let's talk about how to create a simple, effective budget from scratch.

Let's be honest for a second. Does the word "budget" make you want to run for the hills? For years, it did for me. It sounded like a financial diet, a long list of things I couldn't buy and fun I couldn't have. My attempts were always the same: I’d track every penny for a week, feel completely overwhelmed, and then abandon the whole project, feeling more guilty than when I started. It felt like a constant battle between my desire for financial stability and, well, my desire for a spontaneous pizza night.

It wasn't until I reframed the entire concept that things started to click. A budget isn't a cage; it's a roadmap. It doesn't just tell you where you can't go; it shows you how to get where you want to be. Whether that's a debt-free life, a down payment on a house, or just the peace of mind that comes from knowing you’re in control. Creating a budget from scratch is your first, most powerful step toward telling your money where to go, instead of wondering where it went.

And you're not alone in this. With the cost of living being a major topic of conversation across the US, more and more people are looking for clarity. It’s not about becoming a financial genius overnight. It’s about taking small, manageable steps to build a system that works for your life.

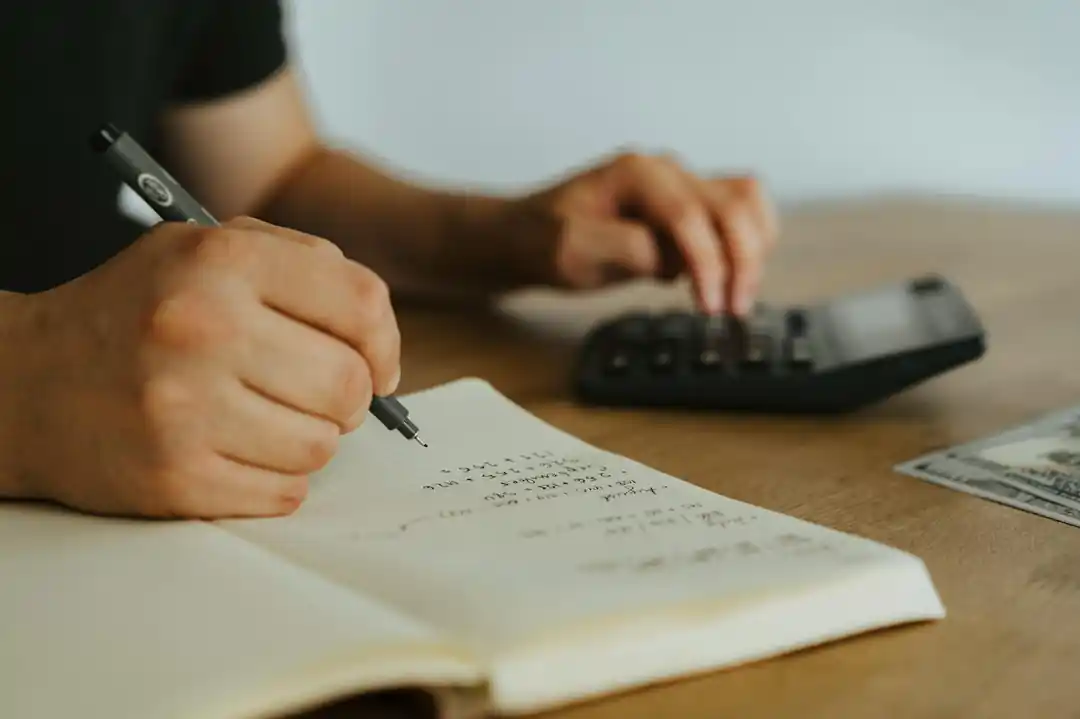

Step 1: The Unfiltered Truth—Track Everything

Before you can make a plan, you need to know what you're working with. This is the most crucial (and often, the most eye-opening) step. For one month, your only job is to become a financial detective. Your mission is to track every single dollar that comes in and every single dollar that goes out. No judgment, no changes, just observation.

You can do this the old-fashioned way with a simple notebook and pen, which can be surprisingly powerful. There's something about physically writing down "–$5.75, coffee" that makes it more real. If you're more digitally inclined, a basic spreadsheet works wonders. Or, you can use one of the many budgeting apps out there like Mint, YNAB (You Need A Budget), or Monarch Money that sync with your bank accounts and automatically categorize your spending.

The goal here is to get a brutally honest baseline. You might think you spend about $300 a month on groceries, but the data might show it's closer to $500. You might discover a forgotten streaming service that's been quietly billing you for a year. This isn't about making you feel bad; it's about gathering the facts. This raw data is the foundation upon which you'll build your entire financial house.

Step 2: Give Your Money a Job with a Simple Framework

Once you have a month's worth of data, it's time to give that money a plan. Instead of getting lost in a hundred different categories, start with a simple, proven method. The most popular and beginner-friendly one is the 50/30/20 rule. It’s less of a strict rule and more of a flexible guide to help you balance your responsibilities and your lifestyle.

Here’s the breakdown:

- 50% for Needs: This is the stuff you absolutely have to pay for. Think rent or mortgage, utilities, essential groceries, insurance, car payments, and minimum debt payments. These are the cornerstones of your budget.

- 30% for Wants: This is the fun stuff! It includes everything from dining out and concert tickets to your Netflix subscription, hobbies, and that new pair of shoes you've been eyeing. This category is vital because a budget that cuts out all joy is a budget you won't stick to.

- 20% for Savings & Debt Repayment: This is where you pay your future self. This chunk of your income goes toward building an emergency fund, saving for retirement, investing, or making extra payments to get out of debt faster.

Take your total after-tax income and calculate what each percentage amounts to. Then, look at your spending from Step 1. How does it stack up? Are your "Needs" taking up 70% of your income? Is your "Savings" category closer to 2%? Don't panic. This is just information. Now you can start making informed decisions.

Step 3: Adjust, Automate, and Be Kind to Yourself

The 50/30/20 framework is a starting point, not a straitjacket. The real magic happens when you start tailoring it to your own life and goals. If you live in a high-cost-of-living city, your "Needs" might be closer to 60%. That's okay. It just means you'll need to adjust your "Wants" category to compensate. If you have an aggressive goal to pay off student loans, you might decide to slash your "Wants" to 15% and boost your "Savings & Debt" category to 35%. You are the CEO of your money—you get to decide the priorities.

Once you have a plan you feel good about, automate it. This is, without a doubt, the single most effective trick to sticking to your budget. Set up automatic transfers from your checking account to your savings account the day you get paid. Schedule your bill payments to go out automatically. By doing this, you ensure your goals are funded and your responsibilities are met before you even have a chance to spend that money elsewhere. It removes the need for constant willpower.

Finally, and this is important, be kind to yourself. You will have weeks where you blow your dining-out budget. An unexpected car repair will pop up. Life happens. A budget isn't about achieving perfection; it's about having a plan to come back to. When you fall off track, don't scrap the whole thing. Just acknowledge it, adjust if you need to, and get back on plan with your next paycheck. This is a marathon, not a sprint.

Building this financial habit takes time, but the sense of control and peace it brings is immeasurable. It’s a journey that transforms your relationship with money from one of anxiety to one of intention. And that is a truly worthy goal.

You might also like

When the Wild Stares Back: What to Do if You Encounter a Mountain Lion

It's a rare, heart-stopping moment. Knowing how to react when you meet a cougar on the trail can make all the difference. Here's how to stay safe.

Beyond 'Everyone': A Small Business Guide to Market Segmentation

Feeling like your marketing is just shouting into the void? Let's talk about how getting specific with market segmentation can change everything for your small business.

More Than Meets the Eye: A First-Timer's Guide to Bangor, Maine

Thinking of visiting Bangor? I went for the first time and discovered a city that's so much more than just a spooky literary landmark. Here's what you can't miss.

Minsk Airport to City Center: Your Stress-Free 2026 Travel Guide

Just landed in Minsk and wondering how to get to the city? I've broken down all the transportation options from the airport to downtown, from budget-friendly buses to comfortable taxis.

Unlocking Serenity: The Quiet Power of a Moon Salutation Yoga Flow

Feeling overwhelmed by the constant hustle? Discover how the gentle, introspective practice of Moon Salutation (Chandra Namaskar) can cool your system, calm your mind, and reconnect you with your inner wisdom.